Building credit is a crucial step in achieving financial independence and opening doors to opportunities such as qualifying for loans, renting an apartment, or even landing certain jobs. If you’re starting with no credit history, the process might seem daunting. However, by following some clear steps, you can establish a strong credit foundation that will benefit you in the long term.

1. Understand What Credit Is and Why It Matters

What Is Credit?

Credit is your ability to borrow money or access goods and services with the agreement to pay later. Your creditworthiness is typically measured by your credit score, which is calculated based on your credit history.

Why Is It Important?

Good credit can help you secure better interest rates on loans, qualify for credit cards, and even save money on insurance premiums. It also demonstrates financial responsibility to potential landlords or employers.

2. Check If You Already Have a Credit History

How to Check

Before starting from scratch, confirm whether you have any existing credit accounts. You can request a free credit report from websites like AnnualCreditReport.com.

Why It Matters

You might unknowingly have a credit history if you’ve co-signed on a loan, had a student loan, or opened a bank account that offered overdraft protection. Knowing your starting point will guide your next steps.

3. Open a Secured Credit Card

What Is a Secured Credit Card?

A secured credit card requires a cash deposit as collateral, which acts as your credit limit. It’s a beginner-friendly way to establish credit.

How to Use It Wisely

- Use it for small, regular purchases like groceries or gas.

- Pay off the balance in full each month to avoid interest charges.

- Never exceed 30% of your credit limit to maintain a healthy credit utilization rate.

4. Become an Authorized User on Someone Else’s Card

How It Works

If a family member or close friend has a credit card with a good history, they can add you as an authorized user. You’ll benefit from their positive credit history without being responsible for payments.

Points to Consider

Make sure the primary cardholder has a good payment history and low credit utilization. Their habits will directly affect your credit score.

5. Apply for a Credit-Builder Loan

What Is It?

A credit-builder loan is designed to help individuals with no credit history. You make fixed payments into a savings account, and once the term is complete, you receive the funds and positive marks on your credit report.

Where to Get One

Look for credit-builder loans at local banks, credit unions, or online lenders.

6. Pay Your Bills on Time

Why It Matters

Payment history makes up 35% of your credit score. Late payments, even on non-credit accounts like utilities or rent, can hurt your credit if reported to credit bureaus.

How to Stay Organized

- Set up automatic payments or reminders for all bills.

- Prioritize paying at least the minimum amount due on credit accounts.

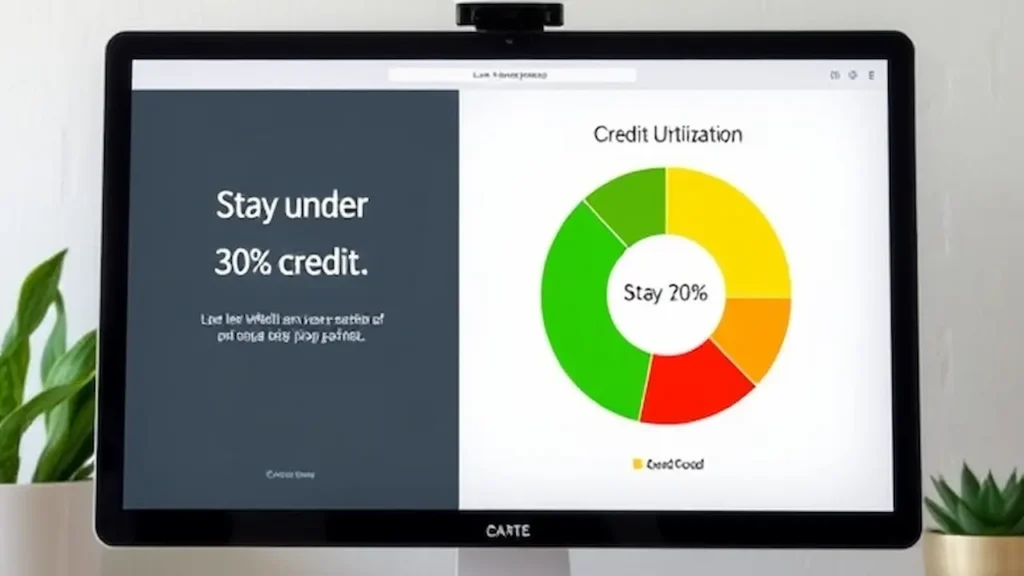

7. Keep Credit Utilization Low

What Is Credit Utilization?

Credit utilization is the percentage of your available credit that you’re using. Keeping it below 30% is essential for a healthy credit score.

How to Manage It

- Pay off your balances in full whenever possible.

- If you have a secured card, consider increasing your deposit to raise your limit.

8. Avoid Applying for Too Many Credit Accounts

Why It’s Important

Each credit application triggers a hard inquiry on your credit report, which can lower your score slightly. Too many inquiries in a short time may signal financial instability.

What to Do Instead

Space out applications and only apply for credit when necessary. Focus on building history with one or two accounts first.

9. Monitor Your Progress Regularly

Why Monitor?

Tracking your credit score allows you to see how your actions impact your credit. It also helps identify errors or signs of fraud.

Tools to Use

Use free credit score monitoring services like Credit Karma or Experian. Check your credit report at least once a year.

10. Be Patient and Consistent

Building Credit Takes Time

Good credit is not built overnight. It requires consistent financial habits over months and years.

Celebrate Small Wins

Each on-time payment and responsible decision contributes to your financial health. Celebrate milestones like reaching a score of 650, 700, and beyond.

Conclusion

Building credit from scratch might feel overwhelming at first, but with a clear plan and consistent effort, it’s entirely achievable. Start small with secured credit cards or credit-builder loans, focus on paying bills on time, and monitor your progress regularly. Over time, these habits will lay the foundation for a strong credit profile, opening doors to greater financial opportunities.

Leave a Reply